Some Of Home Renovation Loan

Table of ContentsRumored Buzz on Home Renovation LoanHome Renovation Loan for DummiesAbout Home Renovation LoanThe 6-Minute Rule for Home Renovation LoanHome Renovation Loan Things To Know Before You Buy

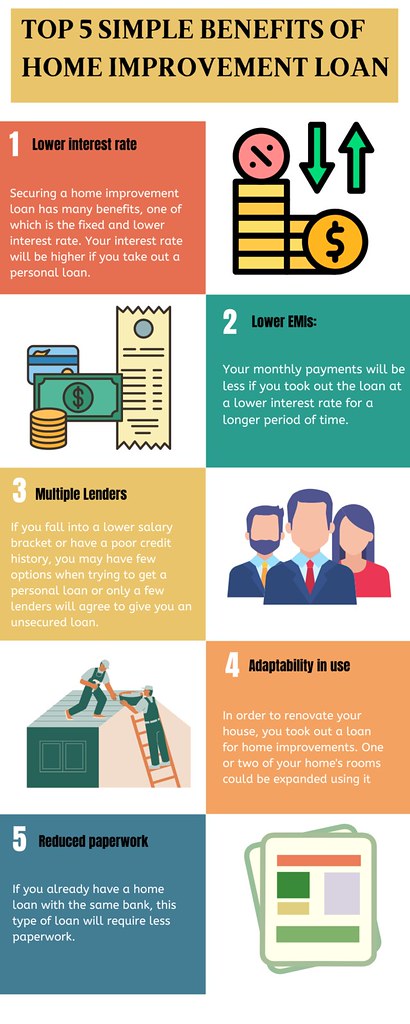

Many business financial institutions provide home renovation financings with very little paperwork needs (home renovation loan). The disbursal procedure, however, is made easier if you obtain the funding from the same financial institution where you previously got a funding. On the various other hand, if you are taking out a financing for the very first time, you must repeat all the steps in the funding application procedureTake into consideration a residence renovation lending if you want to remodel your home and give it a fresh look. With the help of these car loans, you may make your home much more visually pleasing and comfortable to live in.

The major advantages of using a HELOC for a home renovation is the adaptability and low prices (normally 1% above the prime rate). In enhancement, you will only pay passion on the amount you take out, making this a good alternative if you need to pay for your home improvements in stages.

The Ultimate Guide To Home Renovation Loan

The primary disadvantage of a HELOC is that there is no fixed settlement schedule. You have to pay a minimum of the interest each month and this will certainly boost if prime prices increase." This is an excellent financing choice for home renovations if you wish to make smaller regular monthly repayments.

Offered the possibly lengthy amortization period, you could end up paying significantly even more passion with a mortgage refinance compared with other financing choices, and the expenses connected with a HELOC will certainly additionally use. A home mortgage refinance is successfully a brand-new home mortgage, and the rate of interest can be more than your existing one.

Prices and set up prices are typically the same as would spend for a HELOC and you can repay the financing early without fine. Several of our consumers will start their renovations with a HELOC and after that switch over to a home equity loan as soon as all the prices are validated." This can be a great home remodelling financing option for medium-sized tasks.

Not known Incorrect Statements About Home Renovation Loan

Home restoration car loans are the funding option that enables home owners to remodel their homes without needing to dip right into their savings or splurge on high-interest bank card. There are a range of home improvement lending sources readily available to choose from: Home Equity Credit Line (HELOC) Home Equity Lending Home Loan Refinance Personal Financing Bank Card Each of these funding alternatives features distinct requirements, like credit rating, proprietor's revenue, credit line, and rate of interest prices.

Prior to you start of creating your desire home, you possibly need to know the numerous kinds of home improvement loans available in Canada. Below are some of the most usual kinds of home improvement finances each with its own set of attributes and pop over to this web-site benefits. It is a sort of home enhancement funding that enables house owners to borrow a plentiful sum of cash at a low-interest price.

Some Known Factual Statements About Home Renovation Loan

To be eligible, you must possess either a minimum of at the very least 20% home equity or if you have a home loan of Learn More 35% home equity for a standalone HELOC. Re-financing your home loan procedure includes changing your current home mortgage with a new one at a lower price. It decreases your month-to-month payments and reduces the quantity of interest you pay over your life time.

However, it is necessary to find out the possible risks related to refinancing your home mortgage, such as paying more in interest over the life of the loan and expensive costs ranging from 2% to 6% of the car loan quantity. Individual car loans are unprotected financings best suited for those who need to cover home restoration expenditures promptly but don't have enough equity to receive a protected lending.

For this, you may need to supply a clear building and construction strategy you could check here and allocate the renovation, including calculating the cost for all the materials required. Additionally, individual lendings can be safeguarded or unsafe with much shorter repayment periods (under 60 months) and included a higher rates of interest, depending on your credit history and income.

However, for small residence improvement concepts or incidentals that cost a few thousand bucks, it can be an ideal choice. Furthermore, if you have a cash-back bank card and are waiting on your next income to pay for the deeds, you can capitalize on the debt card's 21-day moratorium, throughout which no passion is built up (home renovation loan).

Home Renovation Loan Things To Know Before You Get This

Store financing programs, i.e. Store debt cards are supplied by several home enhancement stores in Canada, such as Home Depot or Lowe's. If you're preparing for small-scale home improvement or DIY projects, such as installing new windows or bathroom remodelling, obtaining a store card through the store can be a very easy and fast process.

Nonetheless, it is crucial to review the terms and problems of the program very carefully prior to choosing, as you might go through retroactive interest charges if you stop working to settle the balance within the time duration, and the rates of interest may be greater than routine home mortgage financing.